How Compound Interest Works

Compound interest can significantly increase your savings over a long period of time. Learn how it works here.

Brandon Canonica

Senior Finance Writer

Brandon is a finance writer and content strategist for ComparisonAdviser. For the past three years, he's written about a variety of topics in the industry, such as insurance, financial advisors, and investing. He specializes in creating detailed, helpful content to assist and inform readers. Brandon is also a co-founder and the COO of RateSonic, a website educating consumers about insurance.

View ProfileTyler Meyer, CFP®

Tyler is a CERTIFIED FINANCIAL PLANNER™ professional and founder of Retire to Abundance and QED Wealth Solutions, a firm specializing in helping people achieve retirement. In addition to being a CFP® professional, he holds the ChFC®, CLU®, RICP®, and FSCP® titles. Outside of his profession, he enjoys visiting National Parks and coaching his kids' athletic teams.

View ProfileThough it might be something easy to overlook in your high school or college math class, compound interest can be a valuable way to grow your savings over a long period. Put simply, it allows your money to build on itself, potentially leading to a much larger sum than you started with.

This article will detail what it is and how it works in-depth. This includes a breakdown of the formula and a visual representation of what it might look like over 30 years. Additionally, we’ll shed light on its benefits and how it differs from simple interest.

What Is Compound Interest?

Compound interest is when interest from your savings makes money over time, even if it’s sitting still. When this happens, your money can grow rapidly, or even exponentially, over time. For instance, imagine you had $10,000 sitting in a savings account at an 8% interest rate and saved $200 per month. After just 20 years, that initial sum would be worth more than $56,000.

“The most obvious benefit of compound interest is the ability to earn more money over time. This is because…not only do you earn interest on your initial investment, but you also earn interest on the accumulated interest over time,” says Mark Buskuhl, founder and CEO of Ninebird Properties, a Texas-based investment firm. He continues, “This compounding effect can lead to significant earnings in the long run.”

It’s important to note that the more time this process can continue uninterrupted, the more your account balance can grow. For this reason, it’s often best to start as young as possible, giving yourself enough time to grow your initial deposit substantially. Buskuhl emphasizes, “The earlier you start investing, the more time your money has to compound and grow.” Because compound interest has the power to turn a small amount of money into a large nest egg, many financial advisors often recommend it as a saving strategy for retirement.

Compound Interest Components

Several factors impact the ability of interest to compound over time. As we noted above, time is one of the most important. However, it’s not the only one. Below is an outline of the components that make up compound interest:

- Principal. This is also known as the initial contribution you had in your account. While it seems important to start with a large sum to earn more, this is not necessarily true. Other aspects, such as your interest rate and time can increase your gains further.

- Interest rate. This is the annual return on your principal. For example, let’s say a $1,000 initial deposit earns 5% per year. At the end of one year, your account balance will be $1,050.

- Compounding frequency. This is the rate at which interest compounding varies and could be daily, monthly, quarterly, semiannually, or annually.

- Time. This is the amount of time your sum has had to grow over a certain period.

Calculating Compound Interest

The most common way to calculate compound interest is using the following mathematical formula:

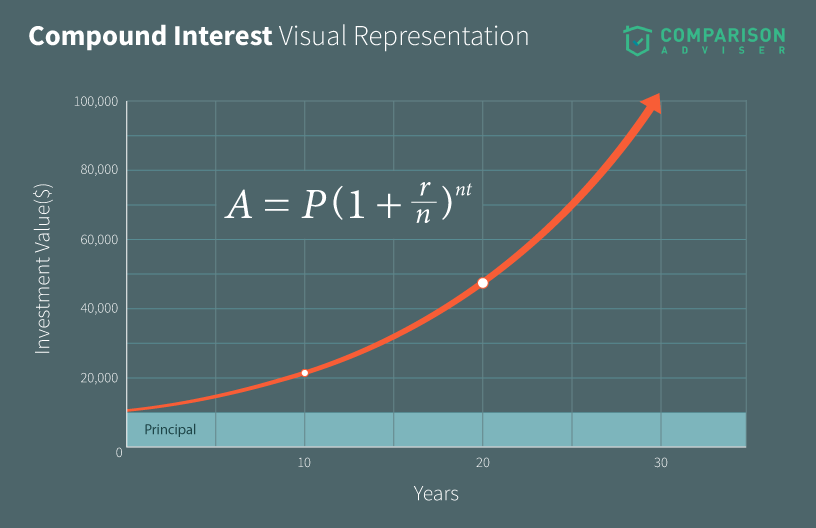

A = P(1 + r/n)nt

Below is a breakdown of each variable:

- A is the total money accumulated after n years, including interest.

- P is the principal amount (the initial deposit of funds).

- r is the annual interest rate (in decimal form).

- n is the number of times that interest is compounded per year.

- t is the number of years the money is invested or borrowed for.

While the formula is the most typical way to figure out how much a sum of money could accumulate over a certain period, another method is the rule of 72. This can tell you how long it will take for an amount of money to double. To use it, you can divide 72 by your interest rate. For example, if your investment had an interest rate of 7%, it would take around ten years to double.

Example of Compound Interest

To illustrate the power of compound interest, consider the following example:

In the above graph, consider that a fictional person named Amy has placed a principal of $10,000 in a savings account and contributes $900 each year (or $75 per month). Her savings account has an annual interest rate of 5%, compounded annually. After about 30 years, the account would be worth about $100,000.

Benefits of Compound Interest

Compound interest’s primary claim to fame is that it can grow a seemingly modest amount of money into a large sum if given enough time. In many cases, it’s as simple as placing money in a high-yield savings account or 401(k) and allowing it to grow.

However, it can also be beneficial when planning for retirement. Per Buskuhl, this is because “it allows you to invest early and earn more over time.” Additionally, he continues, “By starting early and investing consistently, you can build a substantial nest egg for your retirement years.”

Compound interest can also be useful in protecting yourself against inflation. If you have money sitting in an account earning minimal interest, it can lose its purchasing power. But Buskuhl highlights that “compound interest can help mitigate this by providing you with a steady stream of income that keeps up with inflation.”

How It Can Work Against You

Experts often compare compound interest to a snowball rolling down a hill. As it rolls, it grows larger and larger. While this is great when increasing your savings, it can be damaging if you owe a lender.

This is most often the case when you owe money with an interest rate attached, such as with a credit card or mortgage. Todd Stearn, founder of The Money Manual, says, “Many of us have seen compound interest work against us when it comes to credit card debt. The debt snowballs because you start to owe interest on the interest.”

Compound Interest vs. Simple Interest

There are two main types of interest — compound and simple. Because each has a unique function and potential positives and negatives, it’s important to understand their differences.

As mentioned, compound interest grows, often substantially, over time. According to Buskuhl, “This results in faster growth of your investments as compared to simple interest, which only earns interest on the initial principal amount.” It can also be detrimental if you have a debt that you’re not paying on time, since it can grow on itself and make it difficult to pay off.

Conversely, simple interest is only based on the principal investment or loan amount. You can calculate it by multiplying your principal times your rate and the length of your loan or investment term in years. For example, if you had a loan of $22,000 for a new car with an annual rate of 5% on a four-year term, then the total simple interest you’d pay over the four-year term would be $4,400.

Because it doesn’t grow as drastically as compound interest, simple interest is often much friendlier for borrowers. For this reason, Buskuhl observes, “Simple interest is often used for short-term loans or investments, such as car loans or short-term bonds.”

Buskuhl emphasizes considering “that both forms of interest have their own advantages and disadvantages and should be chosen based on individual financial goals and preferences.” Due to its swift growth, compound interest is helpful when growing your assets. On the other hand, simple interest can be more apt for lending than compound interest since it doesn’t drastically increase the size of your loan repayment.

Frequently Asked Questions

Is compound interest a good way to save for retirement?

Compound interest can be effective for saving for retirement. However, it’s worth noting that it can take a long time. This is why it’s often a good idea to start as early as possible, ensuring you have enough of a runway to significantly grow your initial investment or deposit.

What types of accounts are best for accumulating interest?

There are a range of accounts that can be good for compounding interest, including:

- Certificates of deposit (CDs). Per Buskuhl, these can “offer higher returns than savings accounts but require you to lock in your funds for a specific period.”

- Retirement accounts (401(k)s, IRAs, and Roth IRAs). You can earn interest in these and invest at the same time. Additionally, these accounts have tax advantages, allowing you to either withdraw tax-free or on a tax-deferred basis.

- High-yield savings accounts. These are the one of the most common and accessible ways people accrue compound interest.

What’s a common misconception about compound interest?

One of the most typical misconceptions people have about compound interest, according to Buskuhl, is that it can make them “rich overnight.” To debunk this, he says, “While compound interest can result in significant earnings over time, it is not a quick fix to becoming rich. It requires consistency and patience to see substantial growth in your investments.”